If you’re used to investing in stock funds, you may not immediately see the appeal of bond funds.

At first glance, bonds may not seem that different from stocks. As one investor put it: “Bond funds go up and down in price just like stock funds, and many stock funds also pay dividends. What’s the difference?”

While both stock and bond fund prices change, but they do so for different reasons and on a different scale.

Stock fund prices can and have fluctuated wildly; it’s not uncommon for the S&P 500 to move 1-2% in a single day, and the Dow once fell more than -22% in a single day.

Bonds have been far less volatile. The largest single-day drop in the Bloomberg Barclays Aggregate Bond Index was -1.7%. That’s a very different experience. Most people can’t stomach losing a fifth of their assets in a single day.

On a calendar-year basis, the differences are even more stark. Over the past 30 years, the stock market, as measured by the S&P 500 Index, lost as much as -37% in a single calendar year (2008), while the worst year for the Bloomberg Barclays US Aggregate Bond Index was a relatively tame negative -2.6% in 1994.

What about dividend stocks? Aren’t they less risky?

You might think that dividend stocks are less risky than other stocks, and it’s true that funds that buy shares of companies that pay regular dividends may own more defensive companies, like utilities. But defensive stocks are still stocks. They are correlated with the stock market and when stocks fall, they’ll fall, too.

In 2008, for example, the S&P 500 fell -37%. SPDR S&P Dividend ETF (SDY), which invests in dividend-paying stocks, lost -22%, which was better than the S&P 500, but it was still a substantial decline.

Bonds aren’t correlated with stocks: bonds can sometimes gain value when stocks fall, for instance, and that can help limit losses in down markets. In 2009, the bond market gained 5.2%.

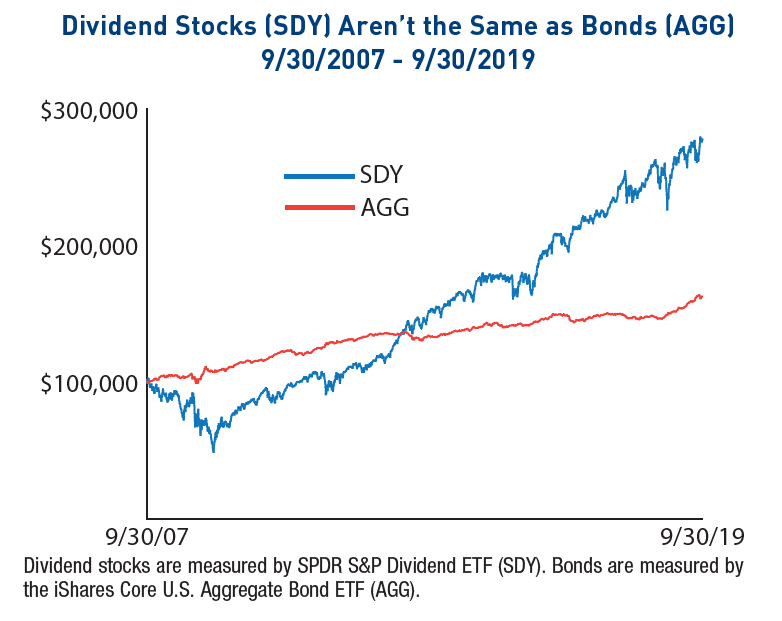

The chart shows the difference between owning an ETF that invests in dividend-paying stocks (SPDR S&P Dividend ETF, SDY) and an ETF that tracks the U.S. bond market (iShares Core U.S. Aggregate Bond ETF, AGG).

In September 2019, these ETFs had a similar yield of about 2.5%, but you can see that they have behaved very differently over time. Investors in SDY faced stock-market-level volatility, including some substantial sell offs. AGG offered a much smoother ride, and it actually made money when stocks fell in the 2007-2009 bear market.

SDY had better returns over this 12-year period, and that’s to be expected. You own stock funds for long-term growth, while bonds are for the lower-risk part of your portfolio, the part of your portfolio that is designed for stability and predictability.

Another thing to keep in mind: Dividend stocks can stop paying dividends, as we saw with PG&E: the California utility abruptly suspended its dividends after devastating wildfires in 2017 and then declared bankruptcy in 2019. If you own the bond of a company that goes bankrupt, you’re first in line, ahead of stockholders, to receive payment.

Should I choose bond funds the same way I choose stock funds?

If you are used to selecting stock funds based primarily on recent returns, you might be inclined to try to choose bond funds the same way. But if you focus on performance alone, you may end up owning a riskier portfolio of bond funds than you’d planned. This can make you feel like you’ve got protection in your portfolio because you own bonds, but if the market declines, you may find that your portfolio is more vulnerable than you’d anticipated.

It makes sense to consider how a bond fund has performed compared to its peers, but performance shouldn’t be your only consideration; you should also be keenly focused on risk. We’ve built this into our Flexible Income approach, by capping the amount we’re willing to invest in riskier types of bond funds.