We’ve talked to a number of investors in the last few months who are planning to retire in the near future, and yet they’re entirely invested in stocks.

If the market keeps going up, this should work out, but what if the market turns?

There are times when it makes sense to dial down risk, if you can, and one of those times is near retirement and your first few years in retirement.

Why? Because this is when you typically have the most money in your retirement accounts, so you have the most to lose if the market tumbles.

A big loss early in retirement can undo years of investment success. It could lead you to postpone your retirement or try to get by on less money in retirement, and that’s not always possible.

You also can’t know in advance what the market will do after you retire. If you happen to retire in a bear market or right before a bear market, you typically have a higher risk of running out of money because you’re withdrawing from your portfolio while your portfolio is losing value.

What if you retire before a bear market?

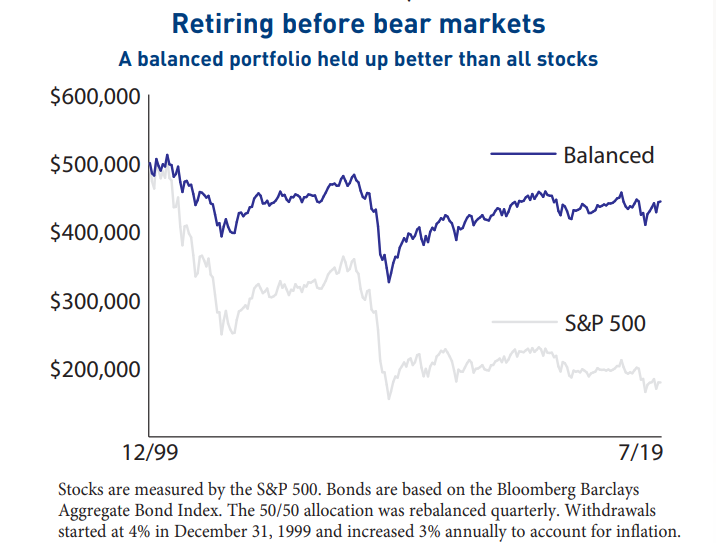

We looked back at how you would have done if you’d retired on December 31, 1999 with a $500,000 portfolio and started taking 4% withdrawals from your account to cover your expenses. We considered two potential allocations: one was 100% stocks and the other was 50% stocks and 50% bonds.

At the end of 1999, the stock market was still in the midst of a strong bull market, and the S&P 500 had posted double-digit gains for five straight years. But in hindsight, it’s clear that this was an unfortunate time to retire since you faced two bear markets in the first decade of your retirement.

If you had invested your $500,000 retirement account entirely in stocks, the combination of bear markets and regular withdrawals took your portfolio down to less than $200,000 by July 31, 2019.

Bonds held up better than stocks during the market declines, so if you’d retired with a balanced portfolio, you ended up with about $443,000 in your account—more than double the amount of a portfolio that owned only stocks.

Your mileage may vary

This is just one example of an allocation during a period that was particularly bad for stocks and unusually good for bonds. However, this 50/50 allocation is consistent with the Trinity study, one of the most well-respected studies on retirement investing.

The Trinity study found that investors who had at least 50% invested in stocks and withdrew 4% from their portfolios for 30 years (adjusted for inflation) had a high likelihood (95%+ probability) of not running out of money during that 30-year period. The study was updated in 2018 to include 63 rolling 30-year periods. We cannot know for certain, however, that people who retire today will enjoy the same chances of success.

This example also kept your allocation and your withdrawals consistent regardless of market action. In reality, many retirees make changes along the way, sometimes cutting back on spending in a year following a market loss.

In our years managing retirement accounts for clients, we’ve found that typically people spend more in the early years of retirement as they’re traveling and checking items off their bucket lists. Their spending eventually plateaus and then picks up again later as health-care costs rise.

Working with an advisor can help you plan for this and invest in a way that helps you address changes in your expenses. Click below to set up a time to talk with a FundX advisor. We'll see if we're a good fit for you, and you're a good fit for us.