How can you invest your retirement assets to make sure that they’ll last your lifetime?

The Trinity study gives you a way to start answering this question.

This study is one of the most well-respected and rigorously tested works on withdrawal rates in retirement. The study was done by three professors—Cooley, Hubbard and Walz—at Trinity University in Texas.

The professors calculated the probability of not running out of money over rolling 15- to 30-year periods using actual historical returns for stocks, bonds, and inflation from 1926 to 1995. (The study was updated in 2009 by these same academics and updated again in 2014 by Professor Wade Pfau of The American College of Financial Services.)

The results give useful guidelines on how to allocate your assets based on your initial withdrawal rate and time horizon.

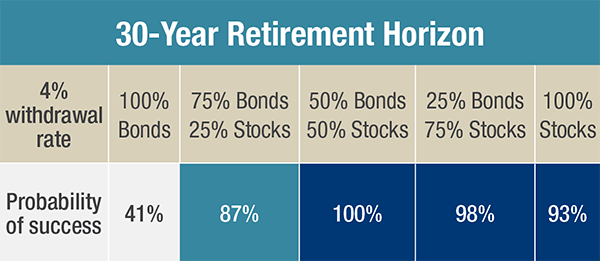

The Trinity study confirmed what’s known as the 4% Rule: investors who invested their retirement portfolio 50% in stocks and 50% in bonds could withdraw an initial 4%, adjusted annually for inflation, and be confident they would not run out of money over 30 years.

The study found that a 4% withdrawal rate was successful 100% of the time over every 30-year period tested. (Interestingly, the study didn’t look at the classic retirement allocation of 60% stocks and 40% bonds.)

Chances of success for five portfolio allocations

The Trinity study considered the probability of success (not running out of money) for four other portfolio allocations ranging from 100% bonds to 100% stocks, shown below.

Investing in a portfolio of 50% bonds and 50% stocks had the highest success rate. There was a 100% probability that you’d have enough money to last 30 years. Getting too conservative, however, really hurt your chances of success. If you’d invested entirely in bonds, however, your success rate dropped to just 41%.

If you owned more stocks, you still had a very good chance of having enough money to last 30 years. It may surprise you to see that owning more stocks didn’t increase your chances of success.

Putting the pieces together

The Trinity study can help you bring together your time horizon, initial withdrawal rate, and your portfolio allocation—three key elements of successful retirement investing that affect your chances of success.

There’s another variable you should consider, and that’s what is an acceptable chance of success for you? Will you feel comfortable selecting a withdrawal rate and an allocation that has historically succeeded 87% of the time? Or do you need a 100% probability to feel confident? That’s a question to talk through with your investment advisor.

Don't have an advisor yet? Click below and let's see if we're a good fit.