Are you investing based on what’s happened in the markets over the long term or what’s happened recently?

Most of us believe that we are investing based on our past experiences as well as long-term trends, but that’s not always the case.

Studies show that we are also strongly influenced by recent events. We can easily and vividly remember what happened in the markets lately, and this leads us to believe that this information is the most important.

Behavioral economists call this “recency bias”, the belief that what happened in the recent past will continue to happen in the future, and this bias is exacerbated in extreme market conditions.

What to watch out for in up & down markets

When markets are regularly hitting new highs, you may become more willing to pay higher prices for stocks, and you may take more risk because recent experience taught us that this pays off. But when markets inevitably change, you may have a harder time staying invested.

You may also end up holding lagging investments too long because you expect them to bounce back. During the tech bust in 2000, many people stuck with technology funds because recent sell-offs had been short-lived and their tech positions had always recovered quickly. You may feel the same way about technology funds or growth funds today when every setback seems to be a buying opportunity.

Down markets can shift your expectations, too. After 2008, many investors steered clear of stocks and stuck with more conservative investments, missing years of the bull market because they feared that the market was on the verge of another major decline.

As you can see, recency bias can lead to costly mistakes, so you’ll want to try to keep it in check.

Three ways to try to counter recency bias in your portfolio

1. Review your portfolio to see if you’re taking more (or less) risk than you’d intended.

Given that people tend to take more risk in up markets, you’ll want to take a close look at your portfolio and see if you’ve begun taking more risk lately.

Consider how much you have invested in stock and bond funds, and then dig deeper to see if you’re mostly invested in diversified stock and bond funds or in more speculative funds. You may find that you’ve been adding more money to higher-risk sector funds, since some of these funds have particularly done well lately, even though your goal is to own broadly diversified funds with market-level risk.

2. See if you are holding funds that should be sold.

Given that we tend to hold on to out-of-favor investments when markets are doing well, you’ll want to be on the lookout for funds that should be sold. It’s tempting to try to wait for funds to bounce back, but remember that lagging funds can stay out of favor for years, while other funds are bringing in better returns.

3. Refresh your memory of market history.

Today, after years of fairly steady gains from stocks, you probably feel pretty comfortable investing in equity funds. Of course, you may have felt that way in 2006 and early 2007, too, when stocks were flying high. But you probably felt much differently about stocks in early 2009, after more than a year of sharp losses and no end to the financial crisis in sight.

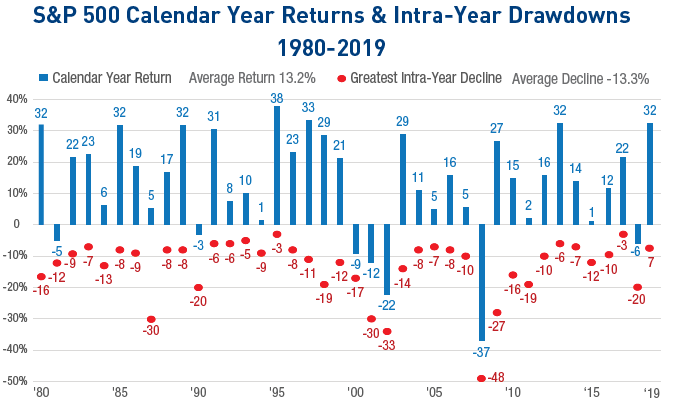

When you look back over many years, you can see that declines and periods of higher volatility are normal and should be expected. Since 1980, the average intra-year decline for the S&P 500 has been about 13%.

The takeaway

While you can’t control what happens in the markets, you can control how you respond to it. When markets are powering forward, it’s easy to get caught up in the excitement. The key to successful long-term investing, however, is to make sure that you’re invested in a way that can help you invest through a wide range of markets, not just this particular one.

If you've been struggling to respond to changing markets, it may be time to consider working with an advisor who can help you stay on track. Click below and let's see if we're a good fit.

A version of this originally appeared on Forbes.